首都圏中古マンションの価格と金利上昇

Prices of Pre-owned condominiums in the Greater Tokyo Area and Rrising

Interest Rates

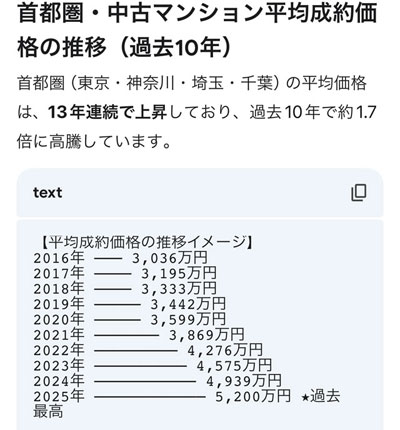

上記の図は首都圏における中古マンション(約60M2)の価格推移であるが、2016年の3,036万円から2025年5,200万円に上昇し、約1.7倍の上昇幅となっている。

これが都心3区になると更にこの倍で、2026年では中古でも1億円を超えると言われる。

これは何時まで続くのか、巷間では現在上昇は止まり、出し値と成約価格には大きな価格差があるとの事。

日銀の以前の政策金利が0.75%であり、これが1.0%になった。たかだか0.25%のアップであるが、今後ともに金利の上昇が続くとすると大きな影響が出てくる。長期に住宅ローンの低金利の時代が続いたが、経済が成長期に入ると4-5%の住宅金利は当たり前になる。

中古マンションの購入者はローン付きで買っている人々が多く、買う際の表面利回りは3-4%程度のものが多いが、表面利回りが3%とすると、実際はこれから管理費、修繕積立金を引くと手元に残るのは2%前後になる。今後管理費、修繕積立金は上昇傾向にあるので、借入金利のわずかな上昇でも赤字になりかねない

このことから、最近の傾向として問題のあるマンションから売り出されている傾向にある。駅から少し遠い、高速度道路に沿って騒音が大きい・排気ガスが多い、入居者の賃貸料金が周りに比べて安い、管理状態が良くないなどから売りに出されてくる。

今後金利の上昇と共に、手取りが赤字になるのを避ける為に、まともな物件が売りに出されてくるので、これからじっくり腰を据えて情報集めをするのが得策になる。株でいう「落ちる剣を掴むな(Don't

catch a falling knife)」という状況になりつつある。

但し、今回の日本の状況は90年代のバブル崩壊時期とは異なり、インフレが激しくなる可能性があり、現金が銀行にある人々は、銀行に預けておくよりはいい物件を見つけて早めに買った方が良いことになる。

Prices of Pre-Owned Condominiums in

the Greater Tokyo Area and Rising Interest Rates

The chart above illustrates the

price trends for pre-owned condominiums (approx. 60 m2) in the Greater Tokyo Area. Prices have surged from 30.36 million

yen in 2016 to 52 million yen in 2025, representing an increase of roughly 1.7

times.

In Tokyo's three central wards,

this growth rate is doubled; it is rumored that even pre-owned units will

surpass the 100-million-yen mark in 2026.

How long can this continue? Word on

the street is that the price surge has already ground to a halt, and a

significant gap has emerged between asking prices and actual contract prices.

The Impact of Interest Rate Hikes

The Bank of Japan's interest rate was raised to 1.0%, and it will be raised

more than 1.0% in the near future. While a 0.25% increase to 1.0% may seem

negligible, a continuous upward trend in interest rates moving forward

will have a profound impact. We have enjoyed a prolonged era of low interest

rates, but as the economy enters a growth phase, mortgage rates of 4% to

5% will become the norm.

Many buyers of pre-owned

condominiums rely on mortgages. At the time of purchase, these properties often

yield a gross return of around 3% to 4%. However, if the gross yield is 3%,

subtracting management fees and repair reserve funds leaves a net return of

only about 2% in reality. Given that management fees and repair reserves are on

the rise, even a slight increase in borrowing rates could easily push owners

into the red.

Current Market Trend:

As a result of these financial pressures, we are seeing a

recent trend where problematic properties are hitting the market first. These

include units that are somewhat far from the station, noisy or exposed to heavy

exhaust fumes along highways, yielding lower rent than surrounding areas, or

suffering from poor management

Strategic Outlook for Buyers

As interest

rates continue to climb, higher-quality properties will likely be put up for

sale by owners looking to avoid negative net cash flows. Therefore, the wisest

strategy right now is to sit tight, take your time, and gather information. The

market is increasingly resembling the stock market adage: "Don't catch a falling knife."

However,

Japan's current economic climate differs from the asset price bubble burst of

the 1990s; there is a strong possibility of intensifying inflation. For

individuals with cash sitting in the bank, finding a high-quality property and

purchasing it sooner rather than later may still be a far better option than

leaving their money in a savings account.

<

To contents in English

|